Education loan repayment can be a huge liability. It’s not just the hefty principal sum that causes the concern. Lack of planning done prior to selecting the loan is another contributor to the stress.

If you are considering taking out a loan or have taken one out already, find out ways that you can repay it to lessen the burden. Understand the various factors that influence loan education repayment in India. It is smart to do your research before you take the loan so that you can plan the repayment.

Here are the main types of lenders and their distinguishing factors. Take the next few minutes how these factors affect your loan repayment strategy.

| Lender kind | Loan type | Moratorium period | Repayment period. |

| Government banks | Secured loans. You have to pledge security | Payment free moratorium period | Repayment period of 12 years to 15 years from the end of your moratorium period |

| NBFCs (Non-Banking Finance Companies) | Unsecured loans, most of the times. No collateral required | Depending on your profile, you have to make partial or full interest payments during the moratorium period. | 10 years as the total loan tenure including the moratorium period. |

| International lenders | Unsecured loans. No collateral or co-signer. | Depending on the lender, you may not have to pay until 6 months after classes end. | Tenure can be anywhere between 7 to 20 years. |

Note – Some government banks may offer unsecured loans.

Plan your education loan repayment so that it does not become an NPA

The NPA scenario:

- You miss EMI payment for 3 consecutive months.

- The bank classifies your loan as a non-performing asset.

- Your collateral falls into risk as it can be seized to recover the full amount.

- You and your co-applicant’s credit score is negatively affected, damaging your ability to borrow money in the future.

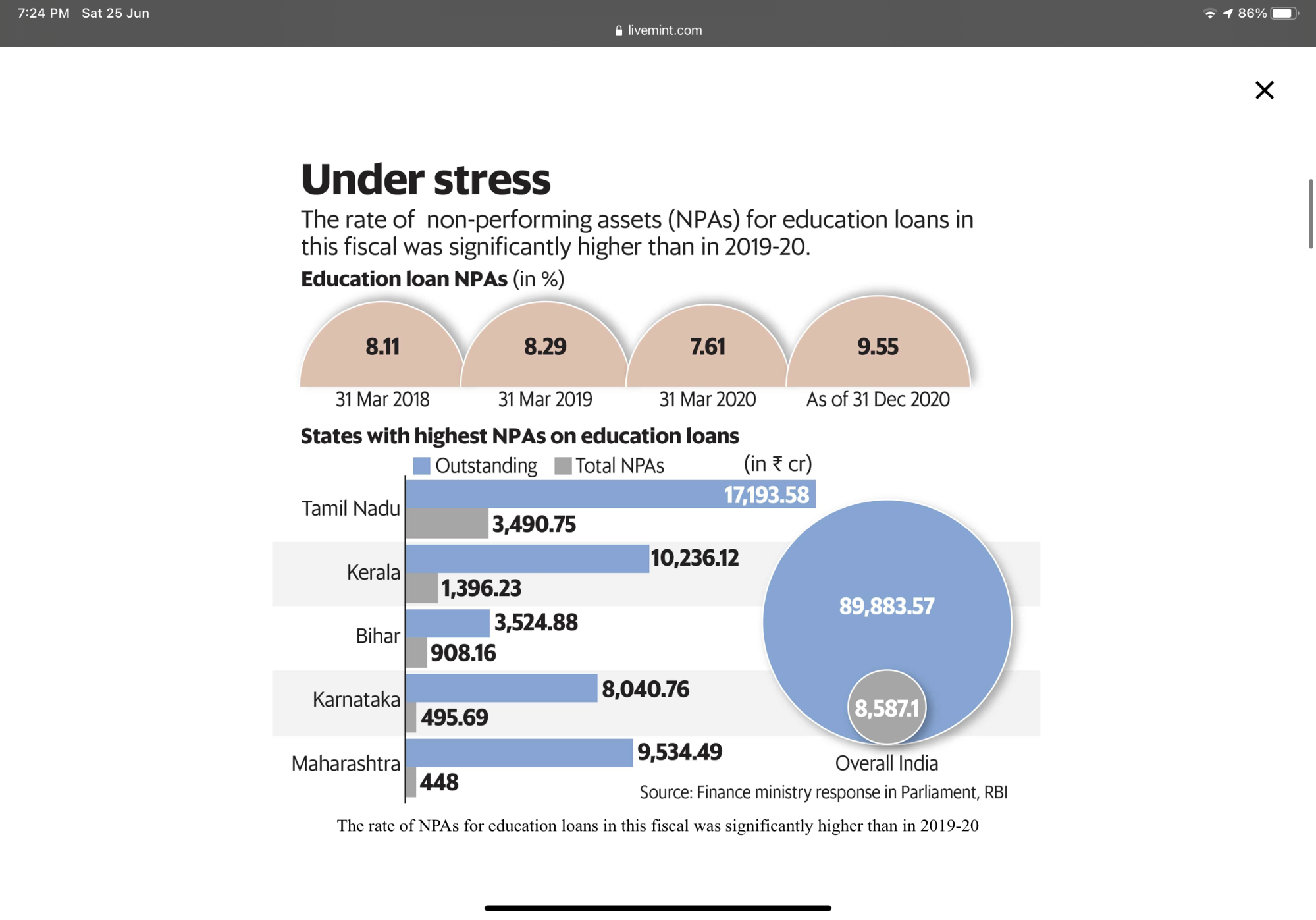

Because of COVID-19 and the consequent financial crisis, education loan NPAs surged to 9.55% in 2019-2020. The statistics discourage students from borrowing as it shows that students were unable to pay their EMI.

However, you don’t have to worry. Education loans for study abroad are a boon. You have to be meticulous about the repayment, that’s all.

Benefits of an education loan from an international lender

If you are confident in your earning abilities, you can borrow from an international lender.

An international lender can give you a load:

- Without a cosigner

- Without any collateral

- With no credit history

This way, your family does not have to risk their assets or credit score funding your education.

GradRight presents an opportunity to access international lenders. With FundRight, you can submit your profile once and receive customized loan offers from public/private sector banks, NBFCs, and international lenders. We currently have 14 lenders and are working to add more lenders.

Determine what you can pay in the moratorium period

You are entitled to a moratorium period on your education loan. This period is also known as the Repayment Holiday. During this period, you don’t have to make any education loan repayments. Most banks do not ask for EMI till after this period.

Moratorium period = Duration of your course + 6 months/1 year.

The time period is between the end of your course and the start of your job. As per RBI, this gap can extend up to a period of one year.

The moratorium period is a perk of education loans. Hence, you shouldn’t take a personal loan to finance your education.

Moratorium scenarios:

| Serial no. | Moratorium option | Advantage | Disadvantage |

| 1. | Pay zero interest during the moratorium (Only Indian government lenders offer this) | Have a financially stress-free education | The interest for the moratorium period will be added to the principal |

| 2. | Pay partial interest during the moratorium | Manageable financial burden | You could apply for a loan transfer later and save money |

| 3. | Pay full interest during the moratorium | No additional interest added to the principal | Can be hectic |

| 4. | Pay EMI during the moratorium | reduces the financial burden for the future | Not being able to pay EMI can cause NPA |

Note: All interest is calculated on a simple interest basis.

Up until around two years ago, you could get a 1% discount on regular payments of the full interest during the moratorium period for education loans from government banks. However, this plan was abandoned a year or so ago. This print might still exist on your loan documents, but it doesn’t apply.

Think about your financial condition. Ask yourself, Can I afford to pay partial or full interest during the moratorium period?

This will help you understand your financial liability and repayment abilities. Depending on that you can plan and repay in an organized manner.

Remember that EMI is different from interest payment. The accrued interest during the moratorium period and course period is added to the principle and repayment is fixed in Equated Monthly Installments (EMI).

Take advantage of subsidized loan schemes

If you haven’t taken a loan already, look for opportunities that can help you save money. For example, government subsidies.

You can find subsidies such as lower interest rates for women, differently-abled or economically weak candidates.

The Vidya Jyoti scheme by Indian Overseas Bank Education Loan is one such example. If you are a female student, you can have a 0.5 percent interest rate reduction on this education loan. The maximum limit for the loan is Rs.40 lakhs.

There are alternatives to government subsidies as well. You might even be able to save more money. For example, FundRight.

The novel bidding platform can help you save up to 23 lakhs in your student loans. You submit your profile and the lenders compete to provide you the best interest rate.

The process is easy and simple and entirely online. So, you don’t have to worry about knowing the ‘right’ people or having connections. You don’t have to wait in long lines.

The lenders are unbiased. This is because you stay anonymous. Your test scores, and background, are not factors that determine the interest rate.

Loan transfer

Regardless of whether you have taken out a loan or not, you can still benefit from a loan transfer.

You can transfer your existing education to a loan to a new lender.

Why would you want to do that?

Once you get a job, your education loan repayment ability improves. Hence, the lender isn’t taking on as much risk.

A new lender can offer a lower rate of interest. This will reduce the EMI you have to pay.

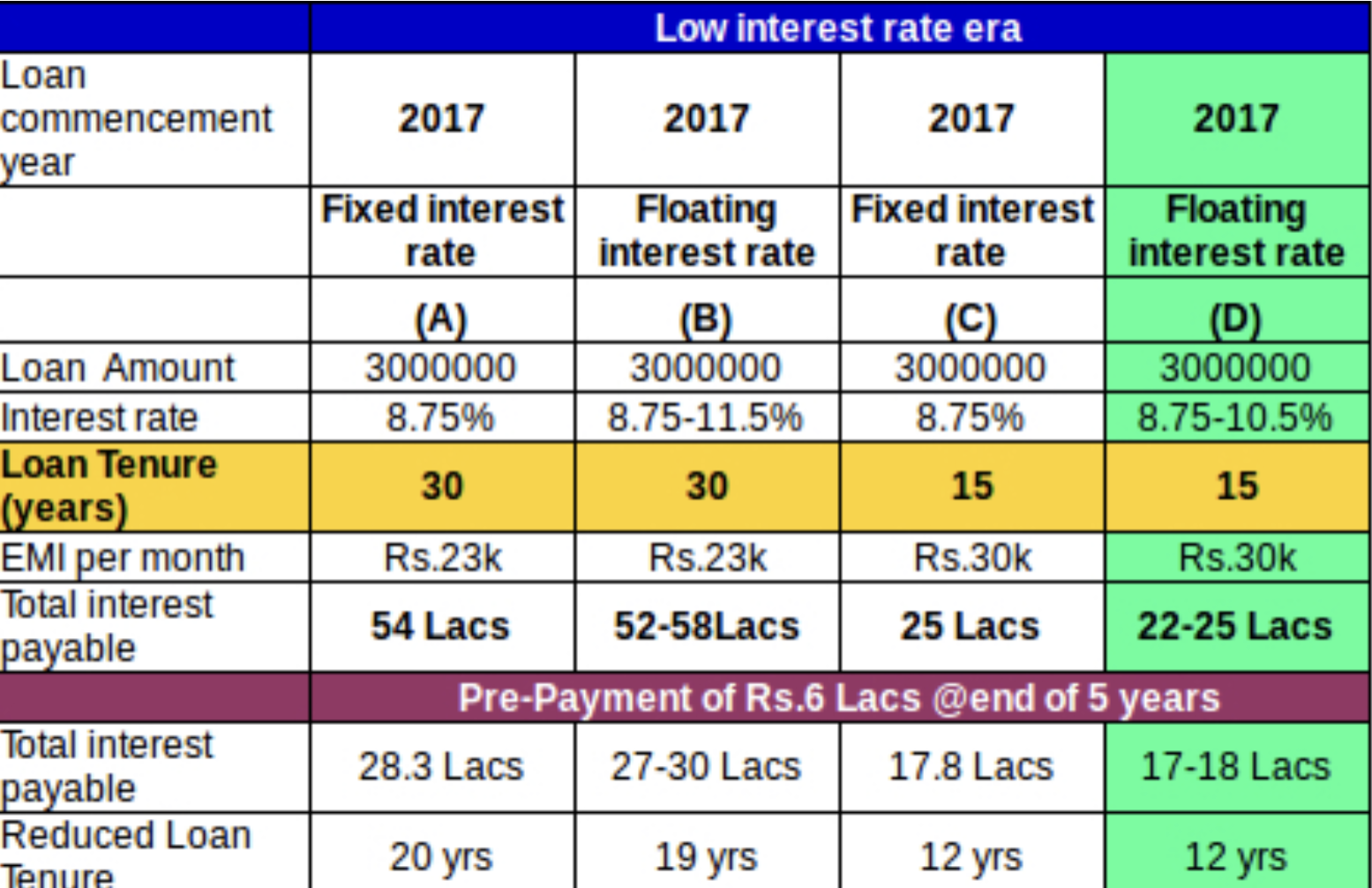

Fixed-rate loans

If you haven’t taken out a loan yet, opt for a fixed rate of interest. This will give you a concrete idea of how much money you have to pay and you can plan accordingly.

A floating rate puts you at a risk of fluctuating interest rates. This can affect your EMIs.

If you have already taken a loan on a floating interest rate, learn about interest fluctuations and be prepared for increments.

Don’t opt for a longer education loan repayment term

Your education loan for studying abroad should not be of a longer tenure. This means that you are paying additional interest.

You usually have 12-15 years to repay your loan after the moratorium period, if you have borrowed from a government bank. Using the entire tenure means taking on an unnecessary financial burden.

Most students are able to repay their loans 5 years after they start their job.

Instead, refinance your education loan. This way you can bargain for a lower rate of interest once you get a job. Your existing interest rate can go down by 1.5-2%.

Save more money by tax deduction

If your parents/guardians are helping you out with your education loan repayment, the tax dedication can be helpful.

The interest that your parents/guardians pay on your education loan can be claimed as a deduction under Section 80E of the Income Tax Act. The rare opportunity is that there is no upper limit of allowed deduction.

The only consideration is that the tenure of your loan should be less than 10 years.

Education loan repayment hacks

Given the experiences of the past students, here are a few ways students were able to repay their loans.

- Have a plan. Research and figure out how you are going to repay your loan before you take one. Search about the average income of your field, and the employment rate of the university you will graduate from to understand your potential earnings. Only then, will you be able to plan other factors such as the tenure of the loan.

- Add the amount of loan, interest rate, and the type of loan to an excel sheet. Keep track of the payments on the sheet.

- Use the education loan repayment calculator facility available on government banks’ official websites to calculate how much amount you are supposed to repay. There should be other calculators for other lending bodies as well.

- There are many variables that determine when you will be able to pay off your goal. However, we recommend that you set a goal year. This will force you to analyze your financial status and keep up with the payments each month.

Even though you have done your research, clarify all the above-mentioned aspects with your lending body.

Here is a checklist of things you should enquire about.

- Tenure period

- Interest rate and the type of interest

- Penalty charges for prepayment

- Payments during the moratorium period, if any

- Any possible schemes that can get you a discount

Selecting a lending body will majorly affect your education loan repayment plan. The less you borrow, the less you have to repay.

With FundRight, you can access a team of financial experts. An unbiased financial advisor will help you compare the multiple offers you receive at FundRight and help you pick one that you can replay easily.