Studying abroad can stretch your wallet.

If you don’t receive a generous scholarship, you need to pay from savings or take an education loan.

Now, loans are a bit tricky to understand. Even though the interest rate is what most students focus on, comparing loans can be more complicated.

In this guide, we focus on enabling you to compare education loans interest rates from the top banks and NBFCs in India.

Think of this guide as a roadmap, helping you compare education loans to figure out which loan is the best companion for your academic journey.

Let’s Compare Education Loans By Different Banks and NBFCs

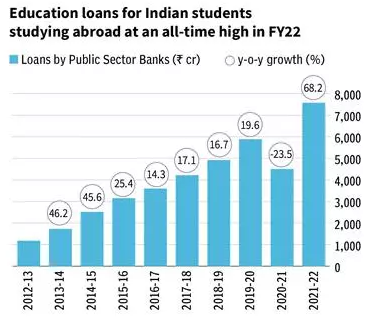

Several banks and financial institutions offer education loans for studying abroad. The graph below shows how lending to students for foreign education has been growing. While the graph shows the data for education loans by public banks only, it reveals the overall trend in the market.

Each loan product comes with its unique terms and conditions, interest rates, and repayment schedules. It’s essential for students to carefully compare education loans before they opt for one.

The following table offers a comparison of interest rates for education loans in India.

| Bank/NBFC | Interest Rate Range | Loan Type | Loan Amount Range |

| State Bank of India | 8.30% to 11.50% | Need-based term loan up to 15 years. | Up to INR 1.5 Crore |

| Punjab National Bank | 8.55% to 11.25% | Need-based term loan up to 15 years. | Up to INR 1 Crore |

| Bank of Baroda | 9.10% to 12.45% | Term loan need-based funding. | Up to INR 80 Lakhs |

| ICICI Bank | 9.50% onwards | Term loan up to INR 1 crore for domestic, and INR 2 crore for international studies. | Up to INR 2 Crore |

| Bank of India | 8.25% to 11.60% | Term loan need-based financing. | Up to INR 1 Crore |

| Bank of Maharashtra | 9.20% to 11.05% | Term loan up to INR 10 lakh in domestic and up to INR 20 lakh for abroad studies. | Up to INR 20 Lakhs |

| Central Bank of India | 8.30% to 11.25% | Term loan up to INR 50 lakh. | Up to INR 50 Lakhs |

| Axis Bank | 13.70% to 15.20% | Customizable loans with flexible repayment options. | Up to INR 40 Lakhs |

| Kotak Mahindra Bank | Up to 16.00% | Custom solutions based on course and institution. | Varies |

| Canara Bank | 7.30% to 9.30% | Need-based term loan. | Up to INR 40 Lakhs |

| Mpower Finance | Starts from 8.00% | No collateral, cosigner-free loans. | Up to $100,000 |

| Prodigy Finance | Variable | Borderless credit, based on future earning potential. | Up to 100% of tuition fees |

A table to compare education loans by India’s top lenders

From SBI to HDFC, ICICI to PNB, we’re here to guide you through the maze of options.

How to choose the best study abroad loans for you?

You have been accepted to study abroad. It is an incredible opportunity for personal and academic growth.

But amidst the excitement, there’s a crucial question: how to fund your dream?

What to look for when you select an education loan? We narrow down the differentiators between loans.

Compare education loans’ tenure

The loan term significantly influences both the monthly payment amount and the total interest paid over the life of the loan.

The longer it is, the lesser the EMI. But a longer term also means they accumulate more interest. This increases the overall cost of the loan.

Let’s understand using an example.

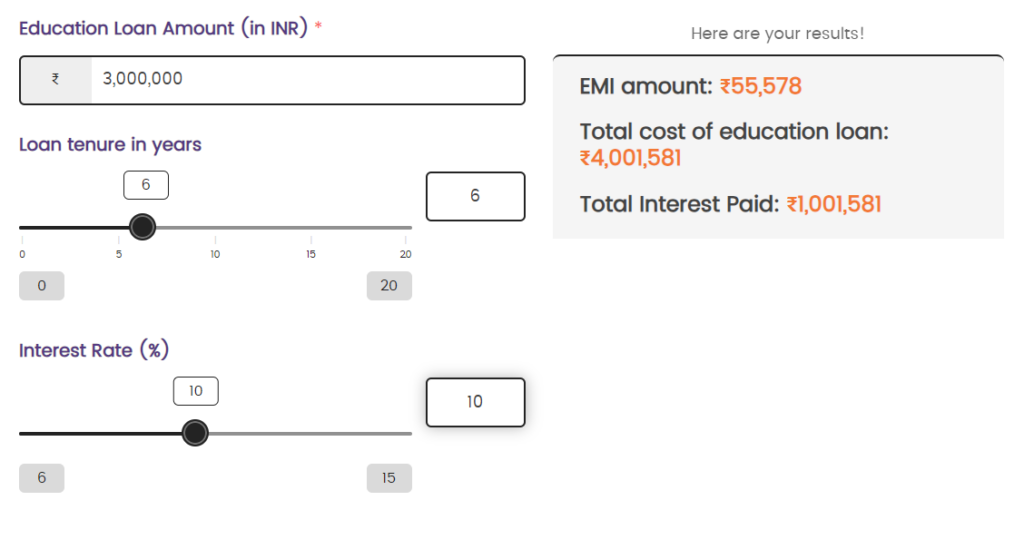

Anil and Aloka both took a loan for INR 40 lakhs.

Both opted for a 10% fixed rate. But Anil wanted to repay in 6 years and Aloka in 12 years.

Anil’s EMI calculation:

Aloka’s EMI calculation:

As we can see, Anil will pay slightly over ₹10 lakhs as interest. Aloka will pay more than INR 21 lakhs. But Aloka pays about ₹20,000 less per month.

So, there’s no black and white answer. For many students, the option to pay a manageable EMI matters more than saving the overall interest they pay on the loan. So, think carefully as to what kind of tenure would suit you before you sign on the dotted line.

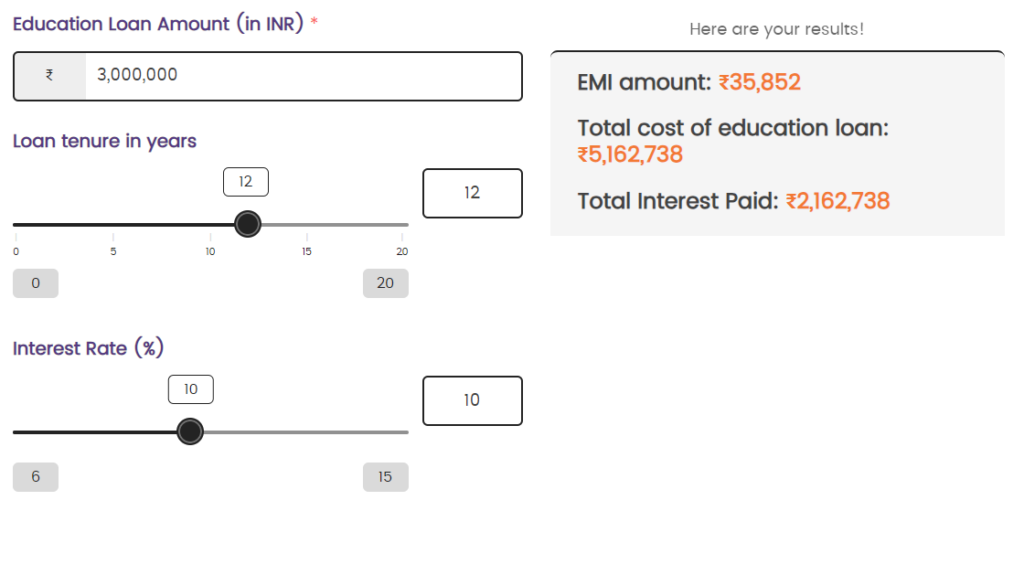

You can use our Education loan EMI calculator to find the tenure that suits you best.

Evaluate collateral

This is the biggest sticking point in most education loans.

After all, banks are running a business. They want to guarantee that they can recover their dues even if the lender fails to keep up with the terms of the contract.

This is why collateral is sought. The collateral may take the form of jewelry, real estate, or certificates of deposit.

In the event of a default on the loan, the collateral can be liquidated to recover the outstanding balance.

But all collateral is not the same.

Gold fluctuates in value. Also, there is the issue of its purity.

House is an illiquid asset. If there are other residents the bank will probably have to go through the legal system to sell the house. Moreover, there is no way to predict the exact price a house would fetch after several years. That is why banks offer no more than half of the value of the house as a loan.

Fixed deposits though are easier to liquidate. That is why most banks prefer FD to other forms of collateral.

Having collateral is not enough. Different banks have different methods of valuing collateral for loans. Choose the one that has the friendliest terms.

Consider guarantor

A bank may require a guarantor. This might be despite collateral. A guarantor steps in and takes responsibility for your loan repayment if you’re unable to meet your obligations.

Guarantors with a strong credit history and stable income boost your loan application’s attractiveness. This reassures the lender and increases your chances of getting approved, particularly when you’re applying for larger loan amounts.

It is best to find a bank that requires either collateral or a guarantor.

Assess moratorium

Let’s talk about the moratorium period. It is a buffer zone built into education loans for students pursuing studies abroad.

This is a grace period when you don’t have to make any loan repayments. It typically covers your study duration (1-2 years) and provides an additional 6 months to help you find a job after graduation.

While the moratorium offers welcome breathing room, it’s crucial to remember that interest continues to accrue during this time. Anil’s 6-year loan (from our example earlier) with a 2-year moratorium is effectively an 8-year loan. More importantly, interest will continue to accrue for Anil during these 2 years.

Some banks may ask for a part of the principal amount to be paid back (by parents) during this period.

Also read: How To Get Education Loan With A Low CIBIL Score

Understanding education loan interest rates for foreign education in India

Fixed and floating interest rates are two ways loan interest rates can be determined.

The fixed-rate remains the same throughout the loan tenure. Floating-rate loans change every six months.

Why does it work like this?

All banks have a Prime Lending Rate (PLR). This is the rate at which they benchmark their loan instruments.

How do banks arrive at this rate? Based on another rate known as the Repo Rate (the rate at which banks borrow from the Reserve Bank of India).

Right now, the repo rate is at 6.5% and the lending rate is at ~10% for most banks.

If the repo rate rises the PLR will also rise, which will affect all loans, and make costlier.

The opposite is also true.

Floating rates change with changes in economic conditions.

Therefore, we have a situation where:

- The repo rate is 6.5%

- PLR is ~10% (this is only available for customers who have perfect credit history and demonstrate better than average ability to repay).

- Educational loan is ~11% at a floating rate.

- The same loan is available for 13% at a fixed rate.

You could either opt for a fixed rate of 13% or opt for a floating rate that changes between 9% and 14% depending on market conditions.

Of course, there might be variations in real life.

Advantages of education loan for abroad

Studying abroad can be an enriching and career-defining experience. But the cost can seem daunting to most of us. The right education loan can be a godsend for a student who aspires to study abroad. Here are all the advantages a good education loan offers.

Covers all aspects of your foreign education

Education loans go beyond tuition fees. They can cover travel costs, and provide for essential study materials. Sometimes even expenses related to program-specific projects or study tours can be met through education loans.

Let’s you focus on studies and not finances

Extended moratorium periods allow you to defer loan repayments until you find employment. This grace period after graduation gives you breathing room to focus on your studies without immediate financial pressure.

Competitively priced as compared to other loan products

Education loans offer lower interest rates compared to other loan options. Plus, you may be able to deduct the interest paid from your taxes. This makes your education even more cost-effective. Of course, you still need to compare education loan rates before you sign the dotted line.

Also read: How To Get An Education Loan Without Parental Support?

How to apply for an education loan in India?

Here is a guide to the education loan application process in India:

- Choose Bank

Select a bank or financial institution offering education loans tailored for international studies, such as SBI, Bank of Baroda, or Canara Bank. You do this when you’ve compared education loan rates from top lenders.

- Check Eligibility

Ensure you meet the eligibility criteria, including academic records, chosen course, age requirements, and Indian citizenship.

- Gather Documents

Compile essential documents like identification, admission confirmation, proof of income, academic transcripts, and, for international studies, visa documentation and acceptance from the foreign university.

- Fill Out Application

Complete the application form accurately with all personal, academic, and financial details.

- Submit Application

Submit your application form and supporting documents either online or at a branch location.

- Interview and Verification

Expect a face-to-face interview to discuss your academic performance and future goals. The bank will also verify your enrollment status.

- Await Approval

After reviewing your application and documents, the bank will decide on loan approval. A guarantor may be required, subject to credit history assessment.

- Receive Your Funds

Upon approval, the sanctioned loan amount will be disbursed directly to your educational institution, either in full or semester-wise.

Now that you’ve learned how to apply for an education loan, you might be wondering if there’s an easier way to connect with the right lenders and secure the best loan terms.

This is where FundRight comes into play.

Why use FundRight?

Applying for an education loan abroad is like untangling a knot.

That’s the frustration FundRight aims to solve.

FundRight aims to create an ethical and transparent bridge between students and lenders.

We wish to reduce the information gap and offer value for all involved.

Here is what sets FundRight apart:

- FundRight helps you find loans and save on interest without visiting a dozen branches.

- No more hunting for a good deal. Banks compete for your loan, ensuring you get the lowest possible interest rate.

- Compare education loan rates, compare terms, shortlist lenders, and then choose one.

- You will have access to expert financial advisors who can help you compare education loans.

- The entire loan application and selection process can be done from the comfort of your home.

- The platform is free for students. There are no unexpected costs or fees involved in the process.

Register on FundRight today and discover the perfect education loan for your needs.

Also Read: A Definitive Guide to Education Loan to Study Abroad

FAQs about education loan for study abroad

When you apply for an education loan, several things come into play. Your academic background, the course and university you’re eyeing, whether you can offer collateral, and if you need a co-borrower or guarantor all play a role.

Lenders check out various aspects of your application. They’re interested in your academic track record, the reputation of your chosen institute, your job prospects after graduation, your potential salary, your credit history, and the type of collateral you can provide.

Your past performance academically matters. Lenders want to see if you have what it takes to complete your course successfully and land a job afterward.

Absolutely! Lenders like to see you aiming for reputable institutes. It makes them more confident about lending to you if your college has a track record of producing successful graduates.

Not always, but having collateral can help. It adds security for the lender and might even get you better terms on your loan.